| February 2011 |

Wake up, Americans

There is a crisis in retirement preparedness in the U.S.

...and it's getting worse, not better.

There is a crisis in the U.S. in the area of retirement preparedness (among others). Moreover, to a great extent, Americans are not even addressing the problem. A recent study by employee benefit consulting firm, Nyhart, found that 81% of workers surveyed will not be financially able to retire at age 65. According to the study, the age at which the average 401(k) participant will be able to retire is 73. The firm concluded that the main reason employees are not able to retire at 65 is that they are not contributing enough money to their 401(k)s.

Unfortunately for some, simply increasing their contributions is not a viable solution. For example, of the 401(k) investors over the age of 55 who are currently not on track to retire at 65, the average percentage of their income they would need to contribute to get on track is 45%! As daunting as the retirement prospects may seem for them, it is even more dire for the 15% of employees who are not even contributing at all to their plan.

Contributing

more $ is not enough -- Investment Assistance is also needed

Contributing more of one's paycheck to their retirement plan -- ideally, the maximum amount allowed -- is obviously crucial to retirement preparedness. However, there is another component to retirement investing that is just as important: the investment management of the plan. That is, what happens to the contributions once they are in the account. And as deficient as many retirement investors are in terms of the amount they contribute, the lack of investment assistance for their account is a much more widespread problem.

Why is investment assistance so important? A contribution to a retirement plan is a one-time event. Yes, it repeated many times and eventually adds up. However, once the contribution is made, that money can be in the account for 10 or 20 or 50 years. The decisions on how that money is invested over that time will determine the success -- or failure -- of one's retirement

With the shift over the years in the U.S. retirement system from predominantly defined-benefit plans (i.e., pensions plans that guaranteed pre-determined payout levels) to defined-contribution plans (i.e., 401(k)'s, etc. where the individual employee controlled the investment of his/her plan), the burden of preparing for retirement has increasingly fallen on each individual. The use of the word "burden" is intentional as the vast majority of individuals are not equipped to manage their investment plans.

This is not a slight. The reality is investing is a full-time job, despite what one hears in commercials from trading firms whose livelihood depends on commissions from their customers trades. Despite being tasked with the responsibility because of the defined-contribution system, retirement investors should not be expected to be able to effectively manage their retirement plan. For starters, they have their own job to tend to. Secondly, they do not have the investment knowledge necessary to make sound decisions. Lastly, and perhaps of greatest importance, without substantial experience most lack the discipline that successful investing requires, leaving them more susceptible to the harmful effects of human nature.

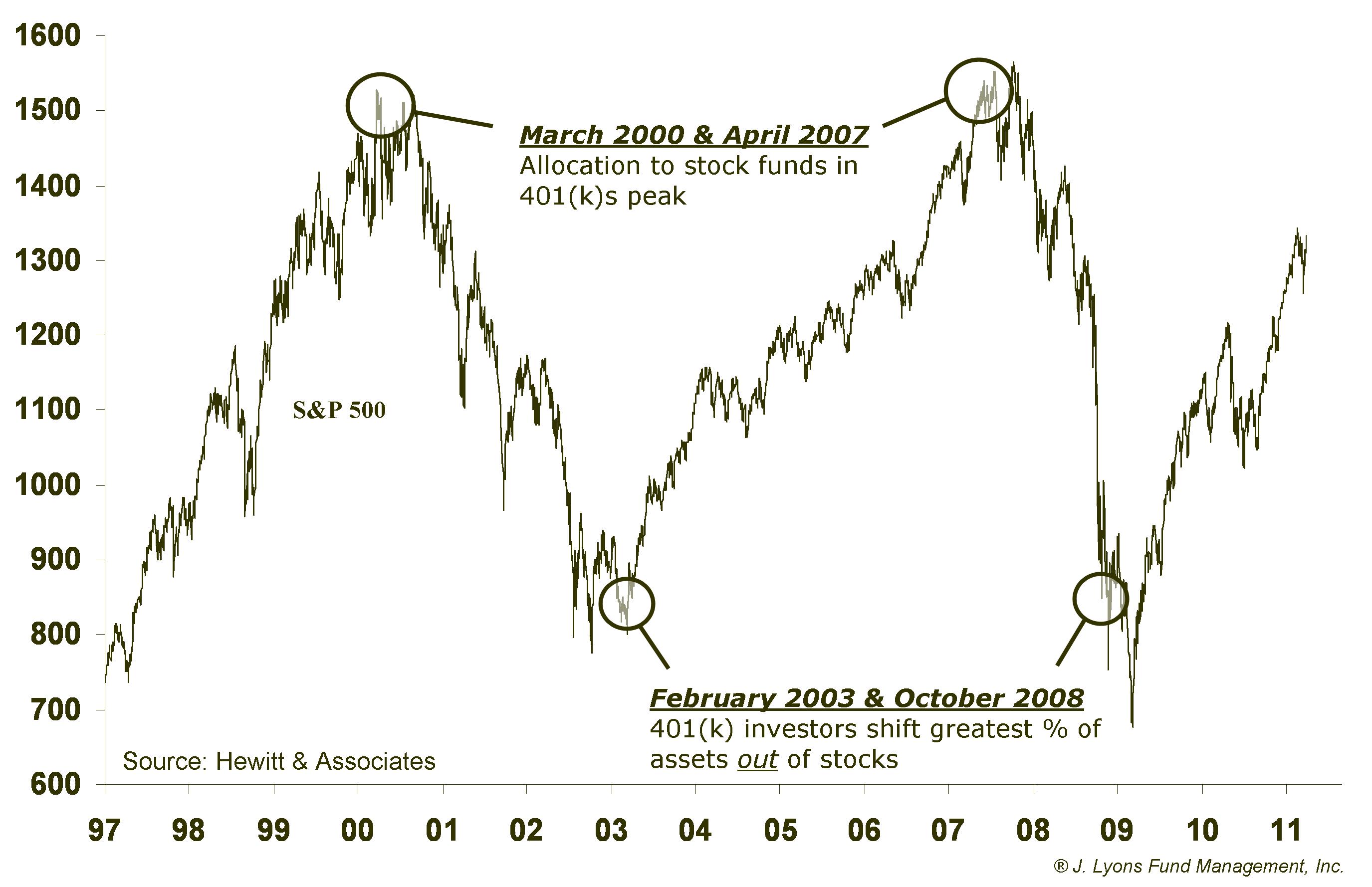

In investing, human nature inclines investors to buy high (greed) and sell low (fear). Evidence bears this out. According to a study by Hewitt & Associates, 401(k) investors' allocation to stock funds peaked in March of 2000 and April of 2007, right near the market peaks. On the flip side, participants pulled the greatest amount of money out of stock funds in February 2003 and October 2008, right near bottoms.

Neither the market nor the economy is likely to bail out your retirement

If retirement investors are hoping for a roaring rebound in the stock market or the economy to bail them out of their retirement predicament, they are going to be disappointed. Besides the likelihood of an ongoing secular bear market (see the December and January Newsletters), the economy has more than its share of headwinds. Take a look at the mess that retirement investors absolutely must contend with for their future well-being:

- The price of corn is up about 100 percent in the past 9 months.

- The United Nations projects global food prices will increase by 30% in 2011.

- Of the 14 million Americans who were officially unemployed in December, 30% had been unemployed for at least a year, according to the Pew Charitable Trusts.

- Approximately 5 million U.S. homeowners are at least two months behind on their mortgages; it's projected that over a million American families will be kicked out of their homes this year.

- According to the Congressional Budget Office, the Social Security system will run a deficit of 130 billion dollars this year.

- Soup kitchen visits are up 24% over the past year according to the U.S. Conference of Mayors.

- The State of Illinois' pension shortage is estimated at $166 billion, or $34,000 per household.

- The U.S. government currently borrows approximately 40 cents of every dollar it spends.

- According to the CBO, the

- The

Investors who don’t think these things will affect their retirement are in for a very rude awakening. And yet, based on observations during a career of providing professional investment help, we are seeing no change in people’s attentiveness to their retirement plans. We're not sure if it is apathy, a fear of the unknown or perhaps a mistrust of the “Wall Street establishment” on the part of investors. Perhaps they can't be blamed for that last item.

What

Should Investors Do?

For

sure, and for starters, investors should investigate sources of

assistance in

managing their retirement savings. As discussed above, most people

simply should not attempt to do

it themselves, considering the time, research and discipline that the

task

requires. It is always difficult and is now made even more so for two

reasons.

First,

no longer is the limited and generic list of investment options (e.g.,

an S&P 500 index fund, a small-cap fund, a growth &

income fund, etc.) offered in a typical retirement plan appropriate or

sufficient.

No, the investment options now must be selected from a global menu and

should

also include not only equities but other investments that, for example,

can

hedge your portfolio against the inflation that is upon us.

Based on our research, and centuries of stock market behavior, buying and holding will continue to be an ineffective strategy in the decade ahead. There very distinctly will be times to be invested and times not to be, as was the case during the past 10 years. We again invite you to read the results of our research in our December and January Newsletters if you have not done so.

We

Can Help

J. Lyons Fund Management, Inc. is an Illinois Registered Investment Advisor, formed in 1985 primarily to assist people with their retirement investing. We now offer two options of investment assistance:

- J. Lyons Fund Management, Inc. provides direct management of retirement investments for our clients. We invite you learn more about our service here on our site or by contacting us. If you are not locked in to a set menu of investment options, we believe this is definitely the better of the two options that we offer as we have access to the great diversity of global investments that we refer to above.

- My401kPro is a low cost subscription site we created to assist 401(k) participants and IRA owners in managing their specific retirement accounts. It is for investors who are confined to a set list of investment funds. This program will assist in maintaining appropriate investment exposure to the markets as well as in selecting the best options to invest in along the way. More details can be found at www.my401kPro.com.

The decision is yours quite obviously. You can continue with the status quo and hope for the best, against great odds. You can follow the stale and misguided buy-and-hold advice that has put most investors in the precarious situation that they now find themselves.Or you can seek real investment help.

John Lyons

President